Market Overview

The global Healthcare Payer Services Market is undergoing a significant transformation, driven by the growing demand for efficient healthcare administration, value-based care models, and digitized service delivery. Payer services refer to the outsourcing of administrative tasks performed by healthcare payers, including insurance companies, government agencies, and employers. These services encompass claims processing, billing and accounts management, member enrollment, customer service, and fraud management, among others.

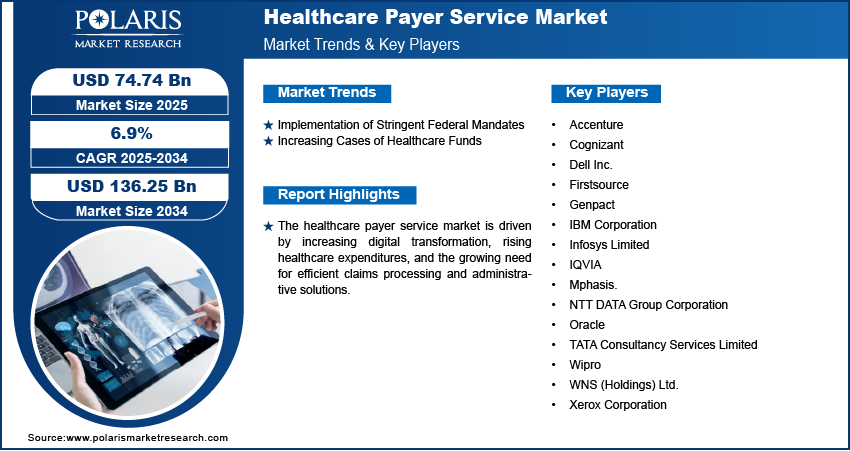

Healthcare payers are under immense pressure to enhance operational efficiency, reduce administrative costs, comply with stringent regulatory frameworks, and deliver seamless customer experiences. To meet these challenges, many are turning to third-party service providers that offer end-to-end solutions leveraging advanced technologies such as artificial intelligence (AI), machine learning (ML), automation, and data analytics.

As healthcare becomes more consumer-driven, payers must invest in services that not only streamline operations but also support personalized engagement. This paradigm shift is positioning payer services as a cornerstone in the global healthcare ecosystem. According to recent market analysis, the healthcare payer services market is expected to witness robust growth, with projections indicating a compound annual growth rate (CAGR) in the high single digits during the forecast period.

Market’s Growth Drivers

1. Increasing Complexity of Healthcare Regulations

One of the primary growth drivers of the healthcare payer services market is the ever-evolving regulatory landscape. Governments around the world are introducing reforms aimed at enhancing healthcare accessibility, affordability, and transparency. Regulations such as the Affordable Care Act (ACA) in the U.S., GDPR in the European Union, and various data protection laws in Asia are compelling healthcare payers to adopt robust compliance mechanisms. Outsourcing services to specialized providers ensures adherence to these regulations, thereby mitigating legal risks and penalties.

2. Rising Demand for Cost Efficiency

The high operational costs associated with managing healthcare plans have forced payers to seek cost-effective solutions. Administrative expenses, which include claims processing, customer support, and enrollment, account for a significant share of total healthcare expenditures. Payer services enable organizations to cut costs without compromising service quality, often by leveraging offshore or cloud-based solutions.

3. Shift Toward Value-Based Healthcare

The transition from fee-for-service to value-based care models is reshaping the healthcare landscape. In this model, providers are reimbursed based on patient outcomes rather than the volume of services rendered. Payers need robust data analytics and performance tracking systems to support this shift. Payer service providers help implement value-based frameworks through population health management, risk adjustment, and quality reporting tools.

4. Technological Advancements

Technological innovations such as robotic process automation (RPA), blockchain, cloud computing, and predictive analytics are revolutionizing healthcare payer services. These tools reduce manual errors, accelerate turnaround times, and provide deeper insights into member behavior and claims data. The adoption of AI-powered chatbots and virtual assistants is also enhancing member engagement and satisfaction.

5. Growing Healthcare Consumerism

Modern consumers expect seamless digital experiences, transparency in billing, and real-time assistance. To meet these expectations, payers are investing in omnichannel support services and personalized communication strategies. Outsourced payer services help organizations manage consumer interactions more efficiently, fostering loyalty and trust.

Browse Full Insights:

https://www.polarismarketresearch.com/industry-analysis/healthcare-payer-services-market

Key Trends

1. Integration of Artificial Intelligence and Automation

AI and automation are increasingly being deployed in payer services to reduce administrative burdens and enhance accuracy. AI algorithms are used for fraud detection, claims adjudication, and member analytics, while automation streamlines routine tasks such as data entry and document verification.

2. Expansion of Cloud-Based Platforms

Cloud computing is enabling scalability, flexibility, and remote accessibility for healthcare payer services. Cloud-based solutions support data sharing across departments, facilitate real-time collaboration, and reduce infrastructure costs. Service providers are leveraging cloud to offer modular and customizable payer solutions.

3. Focus on Fraud Detection and Risk Management

With the rising incidence of healthcare fraud, payers are investing heavily in advanced fraud detection and risk management solutions. Predictive analytics and machine learning are used to identify anomalies and flag potentially fraudulent claims, protecting both patients and organizations.

4. Data Interoperability and Integration

Data silos have long hindered efficient healthcare delivery. Modern payer services emphasize data interoperability, allowing seamless data exchange between payers, providers, and patients. Integration of electronic health records (EHRs), patient portals, and payer databases is becoming increasingly common.

5. Rise of Onshore and Nearshore Outsourcing

While offshore outsourcing remains popular, many healthcare organizations are exploring onshore and nearshore options due to data privacy concerns and the need for real-time collaboration. Service providers in North America and Europe are gaining traction due to their regulatory expertise and linguistic alignment.

Research Scope

The research scope for the healthcare payer services market includes an in-depth analysis of service types, delivery models, end-users, regional dynamics, and competitive landscape. The study aims to evaluate:

- Current market size and forecast

- Technological trends impacting service delivery

- Regulatory and reimbursement landscape

- Competitive benchmarking of key service providers

- Strategic collaborations, partnerships, and mergers

- Regional and country-level growth potential

The scope also extends to assessing how emerging markets in Asia-Pacific, Latin America, and the Middle East are embracing payer services to overcome infrastructure limitations and modernize their healthcare systems.

Market Segmentation

By Service Type

- Claims Management Services

- Claims adjudication

- Claims repricing

- Claims investigation

- Claims settlement

- Enrollment & Billing Services

- Member enrollment

- Premium billing

- Policy management

- Customer Management Services

- Call center services

- Inquiry handling

- Grievance redressal

- Analytics and Fraud Management

- Predictive modeling

- Risk adjustment

- Fraud detection and prevention

- Provider Network Management

- Provider credentialing

- Network development

- Contract management

- HR and Administrative Services

- Payroll management

- Staffing services

By Delivery Model

- Onshore Outsourcing

- Offshore Outsourcing

- Nearshore Outsourcing

Each model comes with its own set of benefits and limitations. Offshore outsourcing offers cost advantages, while onshore models are preferred for regulatory alignment and data sensitivity.

By End-User

- Private Payers (Insurance Companies)

- Public/Government Payers

- Employers

- Third-Party Administrators (TPAs)

Private insurers dominate the market due to their expansive member base and growing focus on customer satisfaction. However, public payers are also increasing their outsourcing expenditures to reduce administrative overheads.

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- U.K.

- France

- Asia-Pacific

- China

- India

- Japan

- Latin America

- Brazil

- Mexico

- Middle East & Africa

- GCC countries

- South Africa

North America currently holds the largest market share, driven by the U.S. healthcare system’s complexity and the adoption of digital technologies. However, Asia-Pacific is emerging as the fastest-growing region due to rising healthcare spending, digital transformation, and medical insurance penetration.

Conclusion

The healthcare payer services market is poised for sustained growth as stakeholders across the value chain seek to optimize operations, navigate regulatory complexities, and deliver superior patient experiences. With the integration of digital technologies and the shift toward value-based care, the role of payer services is expanding beyond administrative support to become a strategic enabler of transformation.

Outsourcing these services not only reduces costs but also provides access to specialized expertise and innovative tools. As healthcare continues to evolve in the face of demographic shifts, rising chronic diseases, and changing consumer expectations, payer service providers will play a pivotal role in shaping the future of health systems worldwide.

More Trending Latest Reports By Polaris Market Research:

Textile Processing Machinery Market

Radiation Dose Management Market