The global pectin market is poised for robust expansion in the coming years, driven by growing consumer preference for clean-label products and increased application in the food, beverage, and pharmaceutical sectors. Pectin, a natural polysaccharide found in fruits such as apples and citrus peels, has gained prominence as a gelling, thickening, and stabilizing agent.

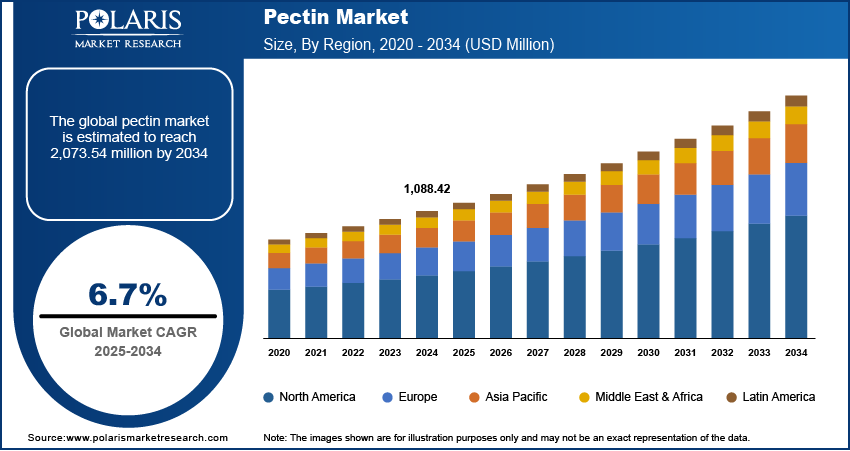

Global Pectin Market size and share is currently valued at USD 1,088.42 million in 2024 and is anticipated to generate an estimated revenue of USD 2,073.54 million by 2034, according to the latest study by Polaris Market Research. Besides, the report notes that the market exhibits a robust 6.7% Compound Annual Growth Rate (CAGR) over the forecasted timeframe, 2025 – 2034

Market Overview

Pectin is a soluble fiber primarily extracted from citrus peels and apple pomace. It has widespread usage in fruit preserves, jams, jellies, and desserts, where it acts as a gelling agent. Beyond the traditional food sector, pectin is also gaining ground in pharmaceutical formulations due to its functional properties such as cholesterol-lowering, anti-diarrheal effects, and its role in gastrointestinal health.

The shift in consumer preference toward natural emulsifiers and texturizers in food and cosmetic products has amplified the demand for pectin. As manufacturers seek alternatives to synthetic ingredients, pectin offers a sustainable, label-friendly solution that aligns with current clean-label trends.

Key Market Growth Drivers

1. Rising Demand for Clean Label and Plant-Based Ingredients

Consumers today are increasingly aware of product labels and are gravitating toward natural, recognizable ingredients. Pectin, being derived from fruits, fits seamlessly into this narrative. The increasing popularity of plant-based ingredients in the food and beverage industry, especially among vegan and vegetarian consumers, is driving adoption across product lines such as yogurts, beverages, dairy alternatives, and fruit spreads.

2. Increased Application in Dairy and Bakery Products

Pectin has become a critical component in dairy and bakery applications, where it enhances texture and stability without altering flavor. It is used to provide mouthfeel in reduced-fat products and improve the shelf life and moisture retention in baked goods. The demand for functional foods and ready-to-eat snacks, particularly in urban markets, has significantly contributed to this growth trajectory.

3. Health Benefits and Nutraceutical Demand

Pectin’s health benefits—such as improving digestion, reducing blood cholesterol levels, and controlling blood sugar—are prompting its inclusion in nutraceuticals and dietary supplements. Furthermore, the aging population in developed markets is increasingly seeking fiber-rich foods that support gut health, making pectin a valuable addition in this segment.

4. Pharmaceutical and Cosmetic Industry Expansion

In the pharmaceutical industry, pectin is used as a controlled drug release agent and as a film-forming agent in topical medications. Its moisturizing and gelling properties also make it a popular ingredient in cosmetic formulations. The crossover of pectin into these non-food sectors is providing a multi-dimensional growth path for manufacturers.

Browse Full Insights:

https://www.polarismarketresearch.com/industry-analysis/pectin-market

Market Challenges

Despite the promising outlook, the global pectin market faces several constraints that could temper its pace of growth:

1. High Cost of Production

Pectin production involves several steps, including fruit sourcing, extraction, purification, and drying, which make it relatively expensive compared to synthetic alternatives. The cost-intensive nature of production, combined with the volatility of raw material availability, poses challenges for small and mid-sized players.

2. Dependence on Seasonal Raw Materials

The industry’s reliance on specific fruit crops such as citrus and apples means that pectin production is vulnerable to climatic conditions, disease outbreaks, and harvest fluctuations. Seasonal variation can result in inconsistent supply and affect pricing, leading to procurement risks for manufacturers.

3. Complex Extraction Processes

The technological expertise and investment required for pectin extraction are substantial. Achieving the desired consistency and grade of pectin for specific applications requires precision and quality control. This technological complexity can act as a barrier to entry for new players in the market.

Market Segmentation:

Pectin Market, Type Outlook (Revenue – USD Million, 2020-2034)

- High Methylated Ester Pectin

- Low Methylated Ester Pectin

- Amidated Pectin

Pectin Market, Raw Material Outlook (Revenue – USD Million, 2020-2034)

- Citrus Peel

- Apple Peel

- Sugar Beet

Pectin Market, Function Outlook (Revenue – USD Million, 2020-2034)

- Thickener

- Stabilizer

- Gelling Agent

- Fat Replacer

Pectin Market, Application Outlook (Revenue – USD Million, 2020-2034)

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Others

Regional Analysis

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing regional market for pectin, with countries such as China, India, and Japan spearheading demand. The rising middle-class population, increasing health awareness, and a growing food processing industry are the key factors propelling market expansion. Moreover, traditional consumption of fruit-based products in the region bodes well for the future of the pectin market.

North America

North America holds a significant share of the global pectin market, driven by mature food and beverage sectors and a strong focus on clean-label and organic products. The U.S. leads in pectin consumption, with major manufacturers catering to demand from dairy, confectionery, and pharmaceutical sectors.

Europe

Europe has traditionally been a dominant player in the pectin market, owing to the presence of abundant raw material sources and a high level of technological expertise in extraction and processing. Countries such as Germany, France, and the Netherlands have well-established food processing industries that use pectin extensively. In addition, European consumers have a longstanding preference for fruit preserves and organic foods.

Latin America and Middle East & Africa (MEA)

In Latin America, Brazil and Argentina are both producers and consumers of pectin, thanks to their citrus industries. The MEA region, although smaller in volume, shows promise due to an expanding food sector and increasing urbanization. Continued investment in food technology and supply chain development is likely to unlock new opportunities in these regions.

Key Companies

The global pectin market is moderately consolidated, with a few major players holding significant shares through long-standing expertise, technological superiority, and integrated supply chains. These companies focus on strategic investments in research and development to enhance product quality, functional range, and application diversity.

Innovation in extraction techniques, eco-friendly production methods, and tailored pectin formulations for specific industrial uses are common strategies for differentiation. Vertical integration, including control over raw material sourcing and processing, provides added value and reliability for large-scale operations.

Companies in the sector are also exploring strategic partnerships with food and beverage producers to develop customized solutions that meet emerging consumer trends—such as reduced sugar content, vegan labels, and enhanced nutritional profiles.

More Trending Latest Reports By Polaris Market Research:

Voluntary Carbon Credit Market

Recycling Water Filtration Market

Solid State Transformers Market